Steel is all around us, from sophisticated defense weapons to railways and buildings, and the COVID-19 pandemic has underscored its critical use in medical equipment. It is the commodity great powers, notably China, may attempt to control and use to coerce other states on international platforms. China’s excessive production of steel is the prime factor in global overcapacity, hurting domestic steel producers in other countries. It also creates unwanted dependencies on Chinese steel, not to mention national security concerns.

Many countries realize this, but fixing the problem is harder than noting it.

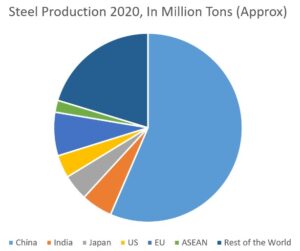

China’s hold over steel, particularly stainless steel, has increased radically in recent decades. In 2020, steel production in China exceeded 1 billion tons, at a time when global steel output was 1.864 billion tons (fig 1) total.

But that is not the complete picture. Chinese companies also produce steel in Southeast Asian countries like Indonesia. Production has shifted to ASEAN countries with the onset of the US-China trade war to reduce dependency on China, but if Southeast Asia’s production of steel, an essential component in manufacturing, were controlled by Beijing, then regional value chains remain vulnerable.

Tariff rows over steel

As succinctly analyzed by Elisabeth Braw for Foreign Policy, China has manipulated the global steel market for years. The Chinese government had long subsidized its steel producers, leading to overproduction. China has likely kept prices of exported steel artificially low, a violation of World Trade Organization (WTO) rules known as “dumping.” The European Union in 2015 imposed anti-dumping duties on China, only to later realize that exports of steel from Chinese companies, produced in Indonesia, were still flooding the market. Once the EU anti-dumping duties were imposed on both China and Indonesia in 2019, Beijing retaliated by increasing tariffs on EU steel imports from 18.1% to over 103%.

Indonesia has the world’s largest nickel reserves but has banned nickel exports as a strategy to boost domestic manufacturing. However, the ban seems to have come (conveniently) after the Chinese company Tsingshan began producing stainless steel in Indonesia. Given Indonesia’s ban on nickel exports, EU steel producers were left in the lurch, whereas the Tsingshan plant in Indonesia continued to produce stainless steel. Tsingshan’s cheap stainless steel exports have rattled markets everywhere. Indonesia was the source of 60% of China’s stainless steel imports in 2018—it had been zero as recently as 2015. The massive export increase is also reflected in a year-on-year difference of 420,000 tons in 2017 to 1.1 million tons in 2018, after which China decided to impose 20% anti-dumping duties on Indonesia.

What are the implications for steel producers like India, Japan, and the United States?

The Trump administration imposed tariffs on all steel imports in 2018, citing a threat to US national security. A 2018 US Department of Commerce report classifies steel as a vital element of national security given its use in “critical infrastructure and national defense,” recommending “immediate action by adjusting the level of imports.” The Biden administration has taken a similar stance, even as Washington and Brussels work toward a settlement.

It became clear, however, that global overcapacity in steel threatens both the American and European steel industries. Japan has also been in talks with the US government since November 2021 to lift curbs on its steel exports under the Japan-US Commercial and Industrial Partnership, and under a newly concluded deal the United States agreed to remove a 25% levy on 1.25 million tons of Japanese steel imports, effective April 1. In its budget for 2022, India removed the countervailing duty, imposed in 2017 on imports of steel from abroad, to bring down steel prices. Given the emphasis on infrastructure in its 2022 budget, and New Delhi’s plans to boost domestic manufacturing under its Make-in-India initiative, steel may be required in abundance.

Modeled on the 2009 Mineral and Coal Mining Law, Indonesia’s ban on mineral exports seeks to channel investment into smelters and processing plants. China has been at the forefront with approximately $30 billion of investment in Indonesia’s nickel value chains. According to the Southeast Asian Iron and Steel Institute, about 59.4 million tons, or 74% of the steel output of ASEAN countries in the next 10 years will come from Chinese projects in these countries. Indonesia will be a leader among them, with an output of 19.5 million tons.

China has several Belt-and-Road-Initiative (BRI) projects in the region, and it is easier to source the essential components of steel for these mega-infrastructure projects from Chinese companies producing locally. However, skepticism over Chinese debt may stall BRI projects in the region. As local consumption slows, ASEAN steel exports will predictably flood international markets even more. For instance, post-China’s anti-dumping duties, Indonesian stainless steel exports to the rest of the world accelerated anxiety among major producers, like POSCO in South Korea, Jindal in India, and local mills in the European Union. In absence of regulatory frameworks, global overcapacity may force steel producers to shut down in many countries and regions like the United States, Japan, and the European Union, in addition to creating dependencies on Beijing.

Possible measures

Despite international pressure, China has had limited success in curbing steel production even after curtailing subsidies. If China, or Chinese companies producing steel in Southeast Asia, continue to dump steel into the international market in this manner, domestic steel industries in many countries will be gravely affected. Given the importance of steel for national security, several countries that view themselves as regional powers in the Indo-Pacific—like India or Japan—and ASEAN nations, which see Chinese maritime expansionism as a threat, may find their autonomy compromised. Even if national security is invoked in such cases to curb imports (like the United States did in 2018), local steel producers will have already suffered substantial damage.

Major steel producing countries may instead coalesce to push the WTO to implement reforms that sufficiently cover the gaps and address ambiguity in dumping regulations, without excluding China from the dialogue in reaching inclusive terms. Large economies like the “Quad” countries (United States, Japan, Australia, and India) might also want to invest in Southeast Asia’s steel sector to ensure diversification and prevent China’s domination of this essential commodity. Since the region is critical for global value chains, preserving its autonomy by diversifying is necessary.

Akash Sahu ([email protected]) is a researcher in Indo-Pacific geopolitics and Southeast Asian studies. He works as Research Analyst at New Delhi-based Manohar Parrikar Institute for Defence Studies and Analyses (MP-IDSA). He looks at traditional and non-traditional security in the Indo-Pacific, balance of power, and inter-state defence relationships in the region.

PacNet commentaries and responses represent the views of the respective authors. Alternative viewpoints are always welcomed and encouraged.